This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

By utilizing key performance indicators in healthcare and healthcare data analytics, prevention is better than cure, and managing to draw a comprehensive picture of a patient will let insurance provide a tailored package. If you put on too many workers, you run the risk of having unnecessary labor costs add up.

Big data and predictiveanalytics will lead to healthcare improvement. Health IT Analytics previously published an excellent paper on some of the best use cases of predictiveanalytics in healthcare. The predictiveanalytics are not designed to replace a doctor’s advice.

The insurance industry is based on the idea of managing risk. To determine this risk, the industry must consult data and see what trends are evident to draft their risk profiles. The twenty-first century offers a lot of exciting innovations when it comes to data processing and analytics. Seeing Into the Future.

In February, we published a blog post on “Using Technology to Add Value in Insurance”. In that post, I referenced Matt Josefowticz’s article – Technology May be the Answer for Insurers, but What Was the Question? , Let’s dive into greater detail on the second lever – Manage Risk Better.

Insurance is no different. Insurance is not something the average consumer thinks about every day but when a life changing event happens, insurance becomes extremely important. It is in this “Moment of Truth” that insurers excel or fail. To provide the best price, the insurer needs to better understand their customer.

In February, we published a blog post on “Using Technology to Add Value in Insurance”. That post, referenced Matt Josefowticz’s article – Technology May be the Answer for Insurers, but What Was the Question? , in which he states that there are only three levers of value in insurance: 1. Manage Risk Better , and 3.

A personal crystal ball that predicts your days ahead is what financial services firms everywhere want. Every day, these companies pose questions such as: Will this new client provide a good return on investment, relative to the potential risk? Is this existing client a termination risk? Will this next trade return a profit?

Ahead of the Chief Data Analytics Officers & Influencers, Insurance event we caught up with Dominic Sartorio, Senior Vice President for Products & Development, Protegrity to discuss how the industry is evolving. Are you seeing any specific issues around the insurance industry at the moment that should concern CDAOs?

With AI, financial institutions and insurance companies now have the ability to automate or augment complex decision-making processes, deliver highly personalized client experiences, create individualized customer education materials, and match the appropriate financial and investment products to each customer’s needs.

For example, insurance companies use cluster analysis to detect false claims, while banks use it to assess creditworthiness. Predictiveanalytics. Predictiveanalytics uses historical data to predict future trends and models , determine relationships, identify patterns, find associations, and more.

In February, we published a blog post on “Using Technology to Add Value in Insurance.” In that post, I referenced Matt Josefowticz’s recent article – Technology May be the Answer for Insurers, but What Was the Question? , in which he argues that there are only three levers of value in insurance: 1. Sell More.

Nancy Casbarro and Deb Zawisa of Novarico recently published a new paper on Data Science in Insurance: Expansion and Key Issues subscription required) that was summarized in this nice little article on Dig-in 3 challenges facing insurers in data science implementation. 1 – Getting business buy-in.

From predictingrisk factors to helping cure disease, Big Data in healthcare is multi-faceted. Through the use of Big Data, opioid usage can easily be tracked and any risk factors for the potential misuse of opioids can be flagged before they happen. The market for big data in healthcare is growing 22% a year.

Consumers are also looking for new machine learning tools to help mitigate their daily risks and solve some of their most perplexing challenges. Data from these accidents is used to train machine learning algorithms to identify correlating risk factors with car accidents. How nuanced can these machine learning risk analyses really be?

Diagnostic analytics uses data (often generated via descriptive analytics) to discover the factors or reasons for past performance. Predictiveanalytics applies techniques such as statistical modeling, forecasting, and machine learning to the output of descriptive and diagnostic analytics to make predictions about future outcomes.

They protect customers, preserve systemic integrity, and help mitigate risks of financial crises. These regulations mandate strong risk management and incident response frameworks to safeguard financial operations against escalating technological threats.

Insurance carriers are always looking to improve operational efficiency. In this post, I’ll explore opportunities to enhance risk assessment and underwriting, especially in personal lines and small and medium-sized enterprises. Utilizing a variety of data sources creates a more accurate picture of risks.

There are several ways that predictiveanalytics is helping organizations prepare for these challenges: Predictiveanalytics models are helping organizations develop risk scoring algorithms. Insurance providers might require them to have adequate safeguards to get compensated for any damages.

Choosing a niche with big data and predictiveanalytics. You can use big data and predictiveanalytics to gauge trends in the music industry and see what will be popular in the future. Insure your business. If you want to become successful in the music industry, it’s essential that you insure your business.

Perhaps the greatest risk to a lending organization is that presented by loan applicants who are unprepared to fulfill the long-term obligation of paying off a loan. Predictiveanalytics can be a crucial piece of the puzzle in supporting the loan approval process and monitoring and managing loans throughout the life cycle of the contract.

The patients who were lying down were much more likely to be seriously ill, so the algorithm learned to identify COVID risk based on the position of the person in the scan. The algorithm learned to identify children, not high-risk patients. The study’s researchers suggested that a few factors may have contributed.

They discuss the impact of the pandemic on enterprises and the need to adopt parallel windows – a short term window to get an enterprise’s operational system up and running as effectively as possible, and a medium-term outlook to mitigate the supply chain shocks and risks. Tune in, and don’t forget to subscribe!

But if they use predictiveanalytics, they can determine how much each case pays out, considering factors as the number of previous cases filled with the same judge. When the risk of recurrence for a malpractice case is high, for example, they can convince the judge to be more generous in rewarding the client.

Matt Josefowticz wrote a great piece recently – Technology May be the Answer for Insurers, but What Was the Question? In this he argues that there are only three levers of value in insurance: 1. Manage Risk Better (aka underwriting and adjusting). Sell More. Cost Less to Operate. Sure, when that makes sense.

Specific Ways Small Businesses Can Use Data Analytics to Resolve Financial Problems. Fraud risks. Small businesses suffer the greatest risks of fraud. A growing number of businesses are using data analytics for fraud scoring. Data analytics tools can help you figure out how to improve your credit score.

How Can Predictive Analysis Tools Help My Hospital or Healthcare Organization? Hospitals and healthcare systems are turning to predictiveanalytics tools to plan and forecast and understand what, when and how to support patients.

The DataRobot AI Cloud Platform can also help identify infrastructure and buildings at risk of damage from natural disasters. With DataRobot, professionals and organizations impacted by natural disasters can solve an array of difficult predictiveanalytics questions and rapidly gain value from their data. Learn more.

This reduces the risk that inaccurate information will be used in your organization’s decision-making, which could result in poor business outcomes. Information management mitigates the risk of errors. Errors can be costly and time-consuming, so the more you reduce the risk of errors, the better. Conclusion.

To keep processing costs low, many insurance carriers have a goal to increase the percentage of their claims that can be processed and decisioned with no human decision-making involved. Perhaps surprisingly, there remains a fair amount of human intervention involved in processing insurance claims.

There are many software packages that allow anyone to build a predictive model, but without expertise in math and statistics, a practitioner runs the risk of creating a faulty, unethical, and even possibly illegal data science application. This almost always results in lack of adoption, and can also expose an organization to risk.

While hiring outside your business’s home country does carry some added risk, you can minimize this through research of international hiring guides and investing in partnerships. Instead, your area of expertise could be selling books, providing insurance, or creating jewelry. Scale Operations According to Cyclical Activity.

Healthcare organizations need a strong data governance framework to help ensure compliance with regulations like the Health Insurance Portability and Accountability Act of 1996 (HIPAA) in the US and the General Data Protection Regulation (GDPR) in the EU. Inaccuracies might also lead to more delays or complications with insurance coverage.

A leading insurance player in Japan leverages this technology to infuse AI into their operations. Real-time analytics on customer data — made possible by DB2’s high-speed processing on AWS — allows the company to offer personalized insurance packages.

It also lets companies provide users with the data they need to complete their jobs more effectively, and even assists in predictiveanalytics. Risk analysts can take advantage of incoming data to continuously modify their risk models and make better calls on insurance, loans, and a variety of other financial decisions.

They offer cheap prices for flight and focus on selling additional bags, meals, complete trip packages, and flight insurance as a way of making money. Predictiveanalytics will be used much more in airline marketing in the months to come. New machine learning technology is making things much easier.

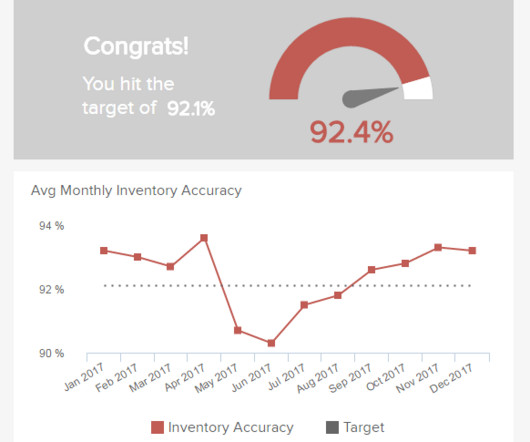

It allows for informed decision-making and efficient risk mitigation. As seen in the image above, these costs can include employee salaries, taxes, insurance, storage, and even the investment opportunities that the business might be losing due to having a lot of resources tight to inventory.

The Fundamental Review of the Trading Book (FRTB), introduced by the Basel Committee on Banking Supervision (BCBS), will transform how banks measure risk. In order to help make banks more resilient to drastic market changes, it will impose capital requirements that are more closely aligned with the market’s actual risk factors.

Clean up with predictive maintenance AI can be used for predictive maintenance by analyzing data directly from machinery to identify problems and flag required maintenance. Maintenance schedules can use AI-powered predictiveanalytics to create greater efficiencies. See what’s ahead AI can assist with forecasting.

Neal Silbert of DataRobot had an interesting post on the DataRobot blog last week – Outcome-Based Claims Assignment: The “New Grail” of Insurance. These review assignments are based on things like the complexity of the claim as well as various risk factors.

AI-enabled robots can work around sensitive organs and tissues, reducing blood loss, infection risk and post-surgery pain. Census Bureau , 28 million Americans didn’t have health insurance in 2020, and even those with insurance don’t always have coverage for every type of screening they need.

It will also give you access to advanced technologies like predictiveanalytics, which can help you get ahead of trends, alert you to staffing issues, skill gaps, and market fluctuations, and provide guidance in an uncertain world. The right analytics can show you how many employees are leaving and why.

The risk is that the organization creates a valuable asset with years of expertise and experience that is directly relevant to the organization and that valuable asset can one day cross the street to your competitors. Organizations that invest time and resources to improve the knowledge and capabilities of their employees perform better.

In a similar vein, in 2018 Forrester split apart its “Wave” for predictiveanalytics products into two distinct Waves. For example, an insurance company could task a team of expert data scientists to work collaboratively in a code-first platform to develop their proprietary claims risk models.

Trying to dissect a model to divine an interpretation of its results is a good way to throw away much of the crucial information – especially about non-automated inputs and decisions going into our workflows – that will be required to mitigate existential risk. Because of compliance. Admittedly less Descartes, more Wednesday Addams.

We organize all of the trending information in your field so you don't have to. Join 42,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content