This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Phase 4: KnowledgeDiscovery. When these two elements are in harmony, there are fewer delays and less risk of data corruption. Phase 3: Data Visualization. With the data analyzed and stored in spreadsheets, it’s time to visualize the data so that it can be presented in an effective and persuasive manner.

Going back to our example of a smart vehicle, what we talked about is only a small part of what knowledge graphs can do in the automotive industry. More and more companies are using them to improve a variety of tasks from product range specification and risk analysis to supporting self-driving cars.

It is a process of using knowledgediscovery tools to mine previously unknown and potentially useful knowledge. It is an active method of automatic discovery. The company can lower the risk value of the red line and monitor the situation in real time. Data Visualization. How BI system solve the problem?

Across industries, this solution unlocks numerous use cases: Research and academia – Summarizing research papers, journals, and publications to accelerate literature reviews and knowledgediscovery Legal and compliance – Extracting key information from legal documents, contracts, and regulations to support compliance efforts and risk management Healthcare (..)

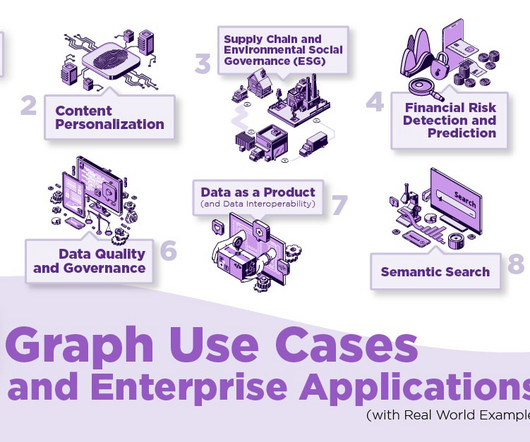

Graphs boost knowledgediscovery and efficient data-driven analytics to understand a company’s relationship with customers and personalize marketing, products, and services. Use Case #4: Financial Risk Detection and Prediction The financial industry is made up of a network of markets and transactions.

One reason to do ramp-up is to mitigate the risk of never before seen arms. A ramp-up strategy may mitigate the risk of upsetting the site’s loyal users who perhaps have strong preferences for the current statistics that are shown. Proceedings of the 13th ACM SIGKDD international conference on Knowledgediscovery and data mining.

This carries the risk of this modification performing worse than simpler approaches like majority under-sampling. Proceedings of the Fourth International Conference on KnowledgeDiscovery and Data Mining, 73–79. Chawla et al. Indeed, in the original paper Chawla et al. 30(2–3), 195–215. link] Ling, C. X., & Li, C.

This is a knowledge that anyone can get, but it would take much longer than optimal. But still, is there a risk that AI could replace people at their workplace? Economy.bg: The pros in this respect are indisputable. How to prepare for a future without employment? Milena Yankova : Will AI replace us? It’s very likely.

These estimates can be useful to make risk-adjusted decisions and explore-exploit trade-offs, or to find situations where the underlying regression method is particularly good or bad. For example, we could use a relatively coarse generalization model for $t$ and rely on calibration to memorize item-specific information.

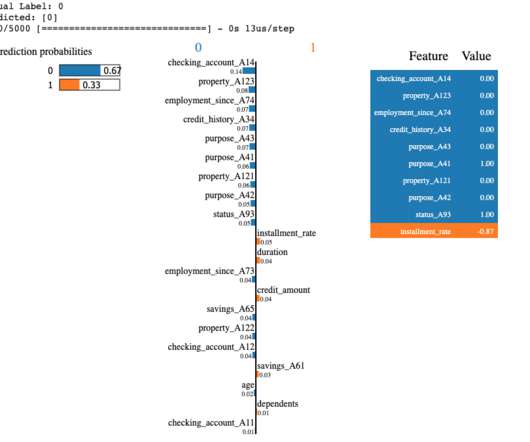

This dataset classifies customers based on a set of attributes into two credit risk groups – good or bad. This is to be expected, as there is no reason for a perfect 50:50 separation of the good vs. bad credit risk. Conference on KnowledgeDiscovery and Data Mining, pp. 1 570 0 570 Name: credit, dtype: int64.

Medicine uses the term “relative risk” to describe effect fraction when referring to the fractional change in incidence of some (bad) outcome like mortality or disease. As noted earlier, effect fractions of 1% or 2% can have practical significance to an LSOS.

We organize all of the trending information in your field so you don't have to. Join 42,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content